The bill doesn’t go into effect until 2027. Is your friend on Medicaid?

1 Like

The changes to the marketplace/exchange begin January 1.

20 Likes

Very sad news for so many people making their livelihoods in the equestrian industry… I’m fortunate that my job supplies insurance. But at my old job I was looking into ACA options when my 26th bday was coming up…

I hope employers can step up but doubtful. It’ll be a big blow to the many self-employed as well.

9 Likes

A lot of people with one or a few employees or seasonal workforce just provide a stipend. That’s worked very well until now in the horse industry and agriculture in general.

3 Likes

The main thing is getting rid of credits that lower the cost of insurance. While this will certainly affect people with low incomes and many people will not be able to afford insurance and the affects will be widespread, it hasn’t “canceled” their insurance immediately. That is why I was asking. I have a lot of issues with this bill but part of fighting it is understanding what it does and does not do. That is why I asked. People in the horse industry are historically low paid and have historically had issues affording insurance and many equine jobs do not come with insurance. The ACA allowed those people to afford insurance and propped up the industry. The issue is two fold. People not being paid enough because we do not value their work. Expensive health insurance that people w low incomes/jobs without insurance can’t afford.

I will add it also affects the enrollment period and automatic enrollment but this is a different barrier and isn’t “cancelling” someone’s insurance immediately.

9 Likes

Graduate students will only be able to borrow $20,500 per year, with a lifetime cap of $100,000. For professional students, including those studying law and medicine, they could borrow $50,000 annually with a lifetime cap of $200,000 (from the link below).

5 Likes

Yes of course. So I suppose if that’s what the friend has there is opportunity to investigate the options

You seem to be imagining some options that I’m not aware of, and I’d find it helpful to know what they are.

17 Likes

I believe there were some recent changes to the laws about medical debt and its effect on your credit, collections etc. my understanding is that they can’t do any of that if you just don’t pay.

Not that I’m advocating not paying your bills but sometimes it is what it is and after a hospital stay or major surgery I can see where some may not be able to pay

There’s a whole marketplace full of them.

I had not heard anything about this part.

But of course they don’t want people to be well educated.

Plus they probably figure that those people can go out in the field and pick produce instead of going to college once they remove all the people who do those jobs now.

23 Likes

Yeah, I’m not sure what other “options” there are for health insurance if you’re not getting it through your employer. I was in this movie until I qualified for Medicare. Remove the subsidies and it’s easily over $1,000 a month plus deductibles.

As for the caps on student loans: So much for all the riders who imagine a life on the show circuit paid for by their career in law or human/veterinary medicine. I suppose if they have access to family money to fund their education they’ll do okay, but for the hoi polloi? The impact of tariffs on showing is probably going to be the least of their worries.

At least these are my opinions. I could be wrong.

15 Likes

Yes, there have been some changes, like a one-year grace period and the increased ability to negotiate a reduced bill. But other than that, if you are employed and don’t “hide” your wages, they will still be garnished. And yes, collections will still come after you. If you’ve got assets, you’re going to have to pay up or be hounded for, I believe, 7 years.

10 Likes

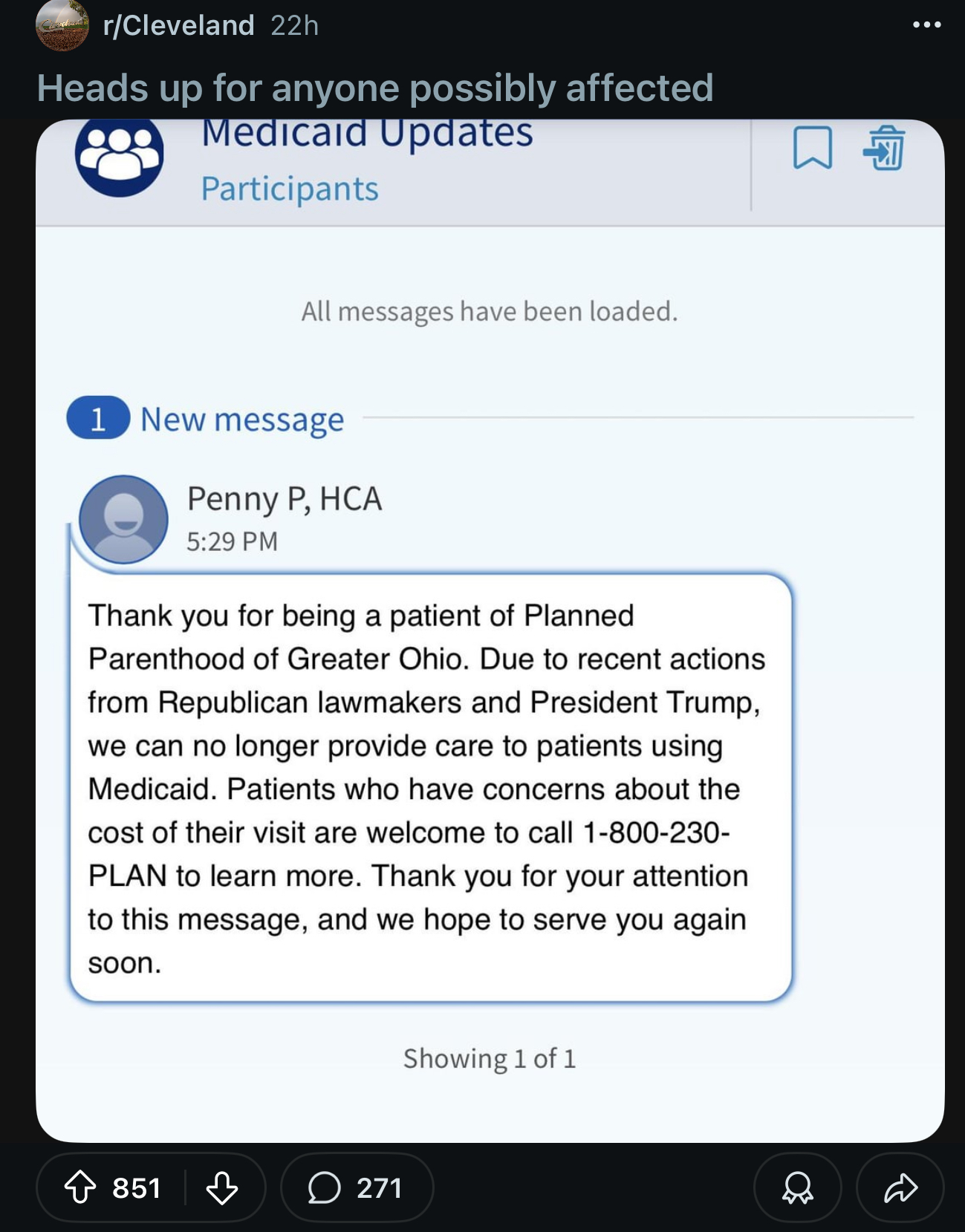

Anyone on Medicaid that utilizes Planned Parenthood is SOL at least in my state, effective immediately: https://www.wkbn.com/news/local-news/youngstown-news/local-planned-parenthood-braces-for-megabills-funding-ban/amp/

Multiple examples of these messages are being shared☹️

14 Likes

The latest from CNN on Trump’s blanket imposition of tariffs on countries that have not yet signed a deal. On the bright side he says money will begin flowing in by August 1, so I expect the kind hearts at Dy’an, Hermes and Kingsland will be joyfully paying their share of the ransom I mean tribute.

7 Likes

Annie10 is a bit of a troll. If you look in the racing forum you will see that logic doesn’t phase them. Best to ignore and not engage. You will not sway their mind.

31 Likes

I’m self employed, Seattle WA. Make enough money therefore no subsidies involved. I have one of the best/most expensive health plans from the exchange and it’s $635/month. I’m healthy and early 40s. I wouldn’t call that affordable but not astronomical considering the high cost of living in my area. I’ve lived here since 2009. Never had an issue getting individual plans via the exchange.

1 Like

Maybe it was because I was older (60-64) and lived in a different state, but I had no subsidies and got the silver or middle plan. $1,400 a month plus a $6,500 annual deductible. Needless to say, I was thrilled when I got old enough to get Medicare and a supplement!

13 Likes

I know. I blame my posts on the 4th of July wine coolers.

19 Likes

Being healthy, fairly young and established enough in your career to be well off, with no dependents, in a wealthy urban area in a blue state with ready access to health care locally is not really the worst case scenario here. I’m not sure what you want people to take from this. Not many in the horse industry are going to relate.

20 Likes